About This Series

The global green transition is often discussed as an environmental challenge. Yet the countries and companies that are emerging as leaders are not only reducing emissions—they are reshaping industries, building new capabilities, and capturing economic value across energy, manufacturing, materials, finance, and trade.

This article is the first in a series by Onch & Co examining the green transition through the lens of economic competitiveness and value creation.

The objective of the series is not to assess climate policies from an environmental perspective alone. Rather, it seeks to understand how different countries are positioning themselves to capture value from the transition, what strategic choices have shaped their outcomes, and what lessons may be relevant for Mongolia.

We begin with China because it represents one of the most consequential examples of how renewable energy policy evolved into a broader industrial and economic development strategy. China's experience demonstrates that the green transition is not only about generating cleaner energy, but also about shaping supply chains, industries, exports, and long-term competitiveness.

Future articles will examine the approaches taken by other countries and regions, exploring how different policy choices, economic structures, and resource endowments have influenced their ability to participate in and benefit from the transition.

The central question throughout the series remains the same:

As the global economy reorganizes around new energy systems and low-carbon value chains, where will value accumulate, who will capture it, and how can Mongolia position itself within this transformation?

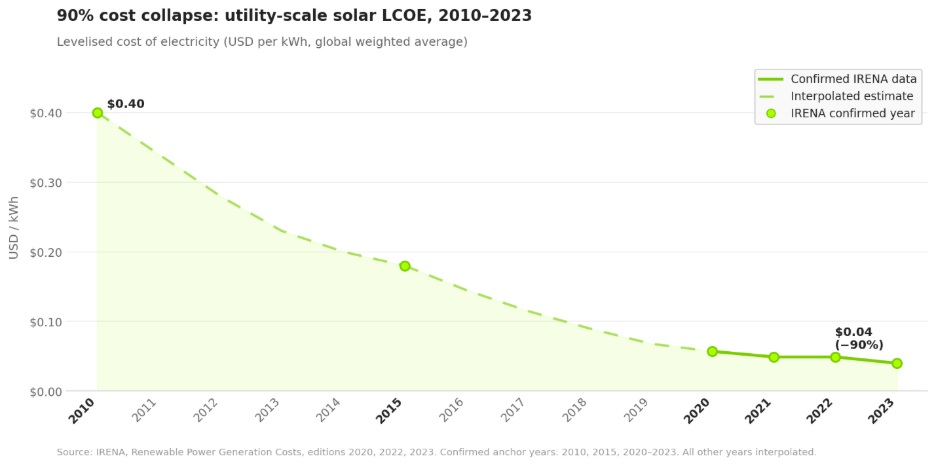

In 2010, generating electricity from utility-scale solar was expensive. The global weighted average cost was approximately $0.42 per kilowatt hour. By 2023, that figure had fallen to roughly $0.04, a decline of nearly 90% in just thirteen years. [1]

Few industrial technologies have achieved cost reductions of this magnitude on a global scale. The decline is often presented as a clean energy success story. It is also evidence of something larger: one of the most significant industrial transformations of the past two decades.

Solar did not become dramatically cheaper simply because the world wanted more renewable energy. Costs fell because manufacturing capacity expanded, supply chains matured, production processes improved, and deployment accelerated. As scale increased, learning accumulated. As learning accumulated, costs fell.

And much of that scale was built in China.

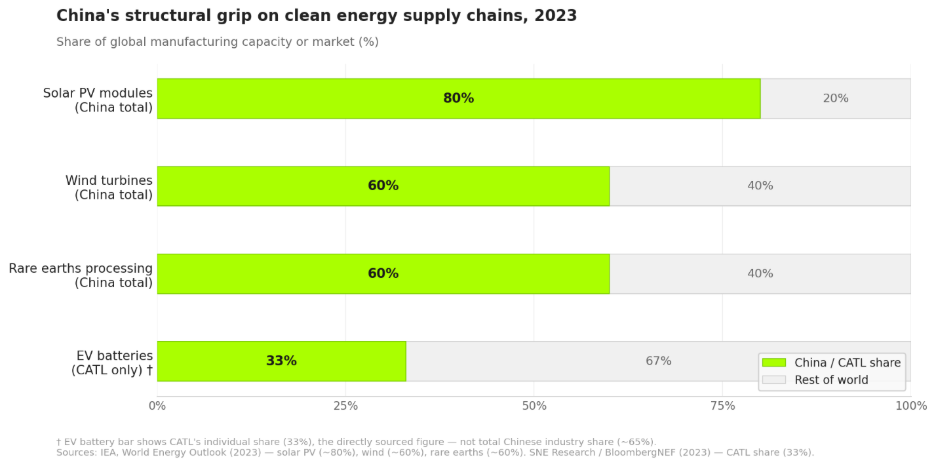

Today, China controls more than 80% of global solar manufacturing capacity across key supply chain stages. [2] Chinese firms accounted for roughly 60% of global wind turbine manufacturing and installations in recent years. China also dominates rare earth processing, accounting for the large majority of global refining capacity used in electric vehicles, wind turbines and advanced electronics.

The same pattern can be seen across batteries and electric vehicles. CATL, founded in 2011, held roughly one-third of the global EV battery market in 2023. [3] Chinese firms collectively account for around two-thirds of global lithium-ion battery manufacturing capacity. BYD surpassed Tesla in total plug-in vehicle deliveries in late 2023, driven by rapid expansion across both battery-electric and hybrid vehicles. [4]

The economic outcomes are now substantial. China's "new three" exports — electric vehicles, batteries and solar products — generated an estimated $140-150 billion in export value in 2023. [5] Estimates of China's broader clean energy economy, including manufacturing, deployment and upstream supply chains, now exceed $1 trillion annually.

These are not isolated company successes. They reflect structural control over key nodes of emerging clean technology value chains.

Understanding how this position was built matters because it reveals something important about the green transition itself.

The transition is not only an environmental shift. It is also a reorganization of how economic value is created across energy, manufacturing, materials, and trade.

China's experience provides one of the clearest examples of this dynamic.

In 2005, China introduced its Renewable Energy Law with objectives that extended beyond emissions reduction. [6] The legislation sought to improve energy security, reduce pollution, and support industrial modernization. Among its provisions was a requirement that grid operators purchase renewable electricity, even when costs exceeded conventional alternatives. [6]

This effectively created what industrial policy scholars describe as a guaranteed “learning market”.

Chinese solar and wind manufacturers had a guaranteed source of domestic demand before their products were globally competitive on price. Every project deployed created opportunities to improve production processes, increase efficiency, and reduce costs.

What followed was a coordinated state-capital system. Policy banks supplied long-term financing to renewable manufacturers. Five-Year Plans designated wind, solar and batteries as strategic sectors. [7] Export incentives supported global market expansion. Industrial clustering concentrated suppliers, manufacturers and exporters in close proximity, creating efficiency gains that compounded over time.

Domestic demand created learning. Learning created scale. Scale created export competitiveness.

China is the most complete expression of this logic, but it is not the only variation of it.

Denmark used early deployment to establish a globally competitive wind industry. Chile is attempting to move beyond raw lithium exports and capture greater value through domestic processing and downstream industries.

Different countries have pursued different approaches, but the underlying principle is similar. During periods of technological transition, value tends to accrue not only to those who adopt new technologies, but to those who build capabilities around them before markets mature.

The challenge is that opportunities do not remain open indefinitely. Some segments of the green economy are already highly concentrated. Solar manufacturing is structurally dominated by a small number of countries and firms. Electric vehicle batteries are following a similar trajectory.

Other areas remain more open. Green hydrogen, advanced materials, traceability infrastructure and premium low-emissions product markets are still evolving. Competitive positions are forming, but many have not yet hardened.

At the same time, market economics and policy frameworks are increasingly moving in the same direction.

Renewables are now the cheapest source of new electricity generation in many markets without subsidy. [8] Electric vehicle ownership costs have reached or approached parity in a growing number of markets and vehicle segments.

The European Union's Carbon Border Adjustment Mechanism (CBAM) entered its definitive phase in 2026, embedding carbon intensity into trade competitiveness regardless of where a product is manufactured. [9] Major financial institutions and development banks are increasingly incorporating climate-related risks into lending and investment decisions, affecting both the cost and availability of capital.

These developments matter because the transition is no longer dependent on policy alone.

Economics, regulation, and capital allocation are increasingly reinforcing one another. When all three begin moving in the same direction, structural change becomes significantly more difficult to reverse.

What this means for Mongolia

Mongolia's experience offers a useful illustration of how policy design shapes transition outcomes.

The Renewable Energy Law of 2007 introduced feed-in tariffs intended to stimulate investment in renewable energy generation. [10] The policy helped create an early renewable energy market and attracted project development interest into the sector.

However, the policy functioned primarily as a generation-support mechanism rather than an industrial development strategy.

This distinction shaped the outcome.

While China used renewable energy policy to create domestic manufacturing capability and export competitiveness, Mongolia's approach focused on expanding generation capacity. As global technology costs declined due to manufacturing scale elsewhere, Mongolia became a purchaser of increasingly affordable technology rather than a participant in the value creation occurring around it.

At the same time, deployment outcomes were influenced by broader system constraints. Generation incentives were not always matched by equivalent investments in grid flexibility, system planning, and market design. Licensing frameworks enabled large project pipelines, while tariff structures became increasingly difficult to reconcile with changing technology costs and system realities.

Over time, tensions emerged between policy design, pricing structures, and the practical capacity of the electricity system to absorb additional generation. By 2019, policymakers had begun transitioning toward competitive auctions as part of a broader effort to improve alignment between renewable energy procurement and system requirements.

The lesson is not that renewable deployment succeeded or failed. Rather, it highlights a broader principle.

Transition outcomes depend not only on whether investment occurs, but on where value is captured within the system. Expanding generation, building industrial capability and creating export competitiveness are related objectives, but they are not the same thing.

The question that remains

If the green transition is reshaping how value is created across energy, manufacturing, materials and trade, then the central question is no longer whether the transition will happen.

The question is where value will accumulate, who will capture it, and how different economies position themselves before those positions become harder to change.

This article is the first in a series by Onch & Co examining how countries, industries, and strategic actors are positioning for the green transition and what these developments may mean for Mongolia. Future articles will explore additional country experiences and examine how policy choices influence the ability to create and capture economic value from the transition.

Onch & Co is a Mongolian consulting and business strategy advisory firm with an ESG practice focused on helping organizations understand how sustainability-related shifts affect competitiveness, investment, and long-term strategic positioning.

Please contact us:

References: