.jpg)

This is no longer a hypothetical question. It is already appearing in audits, investor discussions, and financing processes across Mongolia.

Why?

Because ESG reporting is increasingly becoming a signal of investor confidence. At its core, ESG reflects a company’s ability to identify, manage, and respond to emerging risks. It shows whether management understands the changing business environment and is acting accordingly.

For Mongolian companies aiming to scale, attract international capital, or expand globally, becoming ESG-ready is no longer just about compliance. It is becoming a marker of leadership and operational maturity.

For many companies, the starting point is data.

Take emissions, for example. The issue is often not that emissions were zero, but that they were never measured in the first place. Energy consumption was not tracked in a way that allowed conversion into carbon data. As a result, emissions were not quantified, categorized, or consolidated into a greenhouse gas inventory. The underlying measurement systems simply did not exist.

That is where most Mongolian companies stand today: at the starting point of ESG measurement, while external expectations continue to accelerate.

Do you have the systems to capture the right data, the methodologies to turn it into decision-grade insights, and the internal ownership to ensure consistency and accountability? More importantly, do you have the capability to operate in a business environment increasingly shaped by ESG expectations?

If not, ESG readiness is no longer optional. It is becoming a strategic capability requirement.

Mongolia’s sustainability regulatory landscape is moving quickly from policy intent to implementation.

In 2025, the Government approved NDC 3.0, committing to a 30.3 percent emissions reduction by 2035 and carbon neutrality by 2050. A draft Climate Change Law, including carbon market provisions, is now under development. These signals are already translating into future operational expectations for businesses.

Mongolia has also entered Article 6 carbon market agreements with Japan, South Korea, Singapore (October 2025), and Switzerland (November 2025, during COP30 in Belém)., integrating domestic mitigation outcomes into international carbon finance mechanisms. This creates a direct requirement: emissions must be measurable and verifiable to participate.

On disclosure, the Financial Regulatory Commission has issued ESG reporting guidance and is actively aligning national frameworks with IFRS S1 and S2 through cooperation with the IFC.

Globally, IFRS S1 and S2 are now mandated or adopted in more than 30 jurisdictions. Australia began IFRS S2 aligned disclosure requirements in 2025, with Singapore, Japan, Hong Kong and the UK implementing phased regimes. Even in the United States, California has advanced mandatory climate-related reporting effective January 2026.

For Mongolia, the relevance is structural rather than distant. Major assets such as Oyu Tolgoi are linked to international disclosure environments through Rio Tinto (ASX: RIO). At the same time, ASX listed companies with Mongolian exposure, including Aspire Mining (ASX: AKM), Kincora Copper (ASX: KCC), Resilience Mining Mongolia (ASX: RM1), and Xanadu Mines (ASX: XAM), operate within jurisdictions moving toward more structured sustainability disclosure.

While the scope and timing vary, the direction is clear: disclosure expectations across these capital markets are increasing.

For Mongolian companies with foreign investors, export exposure, or project finance links, this is translating into ESG disclosure becoming an expected part of accessing capital and maintaining commercial relationships.

IFRS S1 and S2 are more demanding than most companies expect. Like financial reporting standards, they are grounded in risk assessment and enterprise value creation, not narrative ESG reporting.

They require companies to show how sustainability related risks and opportunities are identified, assessed, and reflected in financial position, performance, and strategy.

• IFRS S1 focuses on governance, risk identification, and integration of sustainability into enterprise risk management and decision making.

• IFRS S2 focuses on climate, requiring Scope 1, 2, and 3 emissions, scenario analysis, and disclosure of physical and transition risks using defined methodologies and boundaries.

Three areas consistently require structured work:

Governance must show clear accountability, not generic commitment statements. Responsibility across board, executive, and operational levels must be defined, including where governance linkages are not yet established.

Emissions reporting must include methodology, boundaries, exclusions, and calculation logic. The number alone is insufficient without traceability.

Climate risk assessment must be documented even where exposure is low, including assumptions and reasoning.

In practice, the challenge for most companies is not disclosure formatting. It is building the underlying data and decision structures that make disclosure credible.

In anticipation of a rapidly evolving sustainability disclosure landscape, and to proactively strengthen its data readiness and risk management practices in response to increasing international investor scrutiny, Asian Battery Metals PLC initiated the development of its first ESG report. To support this process, we worked with Asian Battery Metals PLC (ASX: AZ9), an Australian-listed exploration company with copper, nickel, graphite, and lithium assets in Mongolia, to align its ESG reporting approach with the phased ASX sustainability disclosure requirements.

A recent testimonial from Asian Battery Metals PLC highlights the impact of the engagement:

“The team demonstrated a strong understanding of international sustainability reporting requirements and provided practical guidance throughout the process. The final report was well-structured, high quality, and valuable in helping us strengthen our ESG disclosures and readiness for evolving IFRS sustainability standards.”

— Business Development Manager, Asian Battery Metals PLC

ABM had already made early progress relative to its stage of development, including initial ESG data collection and identification of material sustainability topics. Our work built on this foundation by aligning existing internal processes more closely with IFRS S1 and S2 disclosure expectations, effectively bridging current reporting practices with emerging mandatory requirements under the ASX sustainability framework.

In the IFRS S1 & S2 aligned report, the following new parts were added:

• Basis of report preparation

• Formal reporting boundary definition (operational and GHG boundaries)

• Materiality assessment framework

• Governance framework and accountability mapping

• Linkage to general purpose financial reporting

• Explicit time horizons (short, medium and long term)

Taking governance as an example, existing practices were restructured into a defined accountability framework across Board, executive and operational levels. Where linkages, such as climate-related remuneration, were not yet formalized, this was explicitly disclosed. IFRS S1 requires transparency around assumptions, limitations and areas where practices are still under development.

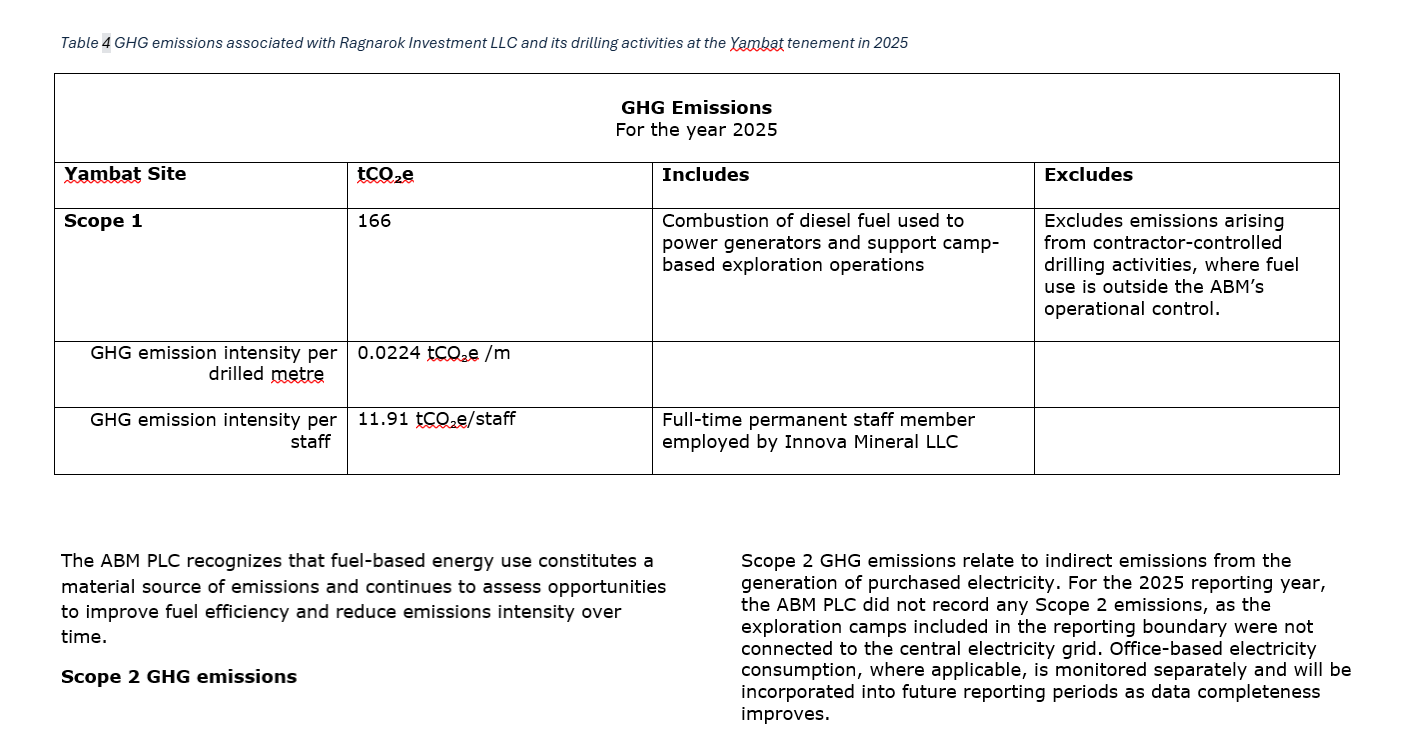

For GHG emissions, Scope 1 data was derived from underlying fuel consumption records (diesel, petrol and LPG) and structured in accordance with the GHG Protocol Corporate Accounting and Reporting Standard, including defined emission factors and calculation methodology. Scope 2 emissions were reported as nil due to the absence of grid electricity consumption across operational sites, with full methodological disclosure provided.

Most Mongolian companies are earlier in the process than ABM. Many do not yet have a greenhouse gas inventory. That is not a reason for the delay. It is a reason to start now, before investor expectations and disclosure requirements become more detailed and difficult to meet.

This matters because IFRS S1 and S2 are not simply reporting frameworks. They are management frameworks. They assess how companies identify, measure, and manage sustainability-related risks and opportunities, and whether those considerations are reflected in strategy, operations, and financial decision-making.

In practice, investors are not only reviewing emissions numbers or disclosure volume. They are evaluating whether management understands emerging risks, has the systems to generate reliable data, and can adapt the business to a changing operating environment.

For boards and investors, this has become an important signal of business quality and readiness. Companies that can demonstrate structured ESG risk assessment, clear methodologies, and consistent internal processes increasingly position themselves as more investable, resilient, and prepared for long-term growth.

The path forward is practical and sequential: understand your current position, establish the necessary measurement systems, and build transparent, IFRS-aligned disclosures over time.

The first ESG report does not need to be perfect. But it should demonstrate that the company is measuring what matters, building internal capability, and preparing itself for a business environment increasingly shaped by sustainability expectations.

Onch & Company has over 20 years of experience in audit, tax, and advisory, and is developing ESG advisory capabilities aligned with IFRS S1 and S2.

Our work focuses on IFRS readiness, including gap assessments, emissions structuring, governance mapping, and disclosure preparation grounded in financial reporting discipline.

We work with existing client data, identify structural gaps, and build toward audit-ready ESG reporting baselines.

Over time, this capability will extend into ESG data systems and tools that support ongoing reporting and decision making.